By Janice DeMonsi, Director of Recreation Santa Clara University, Co-Chair of NIRSA’s Strategic Values Commission for Sustainable Communities

Has your campus recreation program made a commitment to operating sustainably? Do you want to learn how to make it easier to buy green? For example, simple changes—like purchasing recycled paper, green cleaning supplies, or fair trade sports balls—can help make your program more ecologically-friendly.

Who knows? You may be surprised to learn that your program is already engaging in some sustainable purchasing practices.

Using a framework to guide sustainable practices

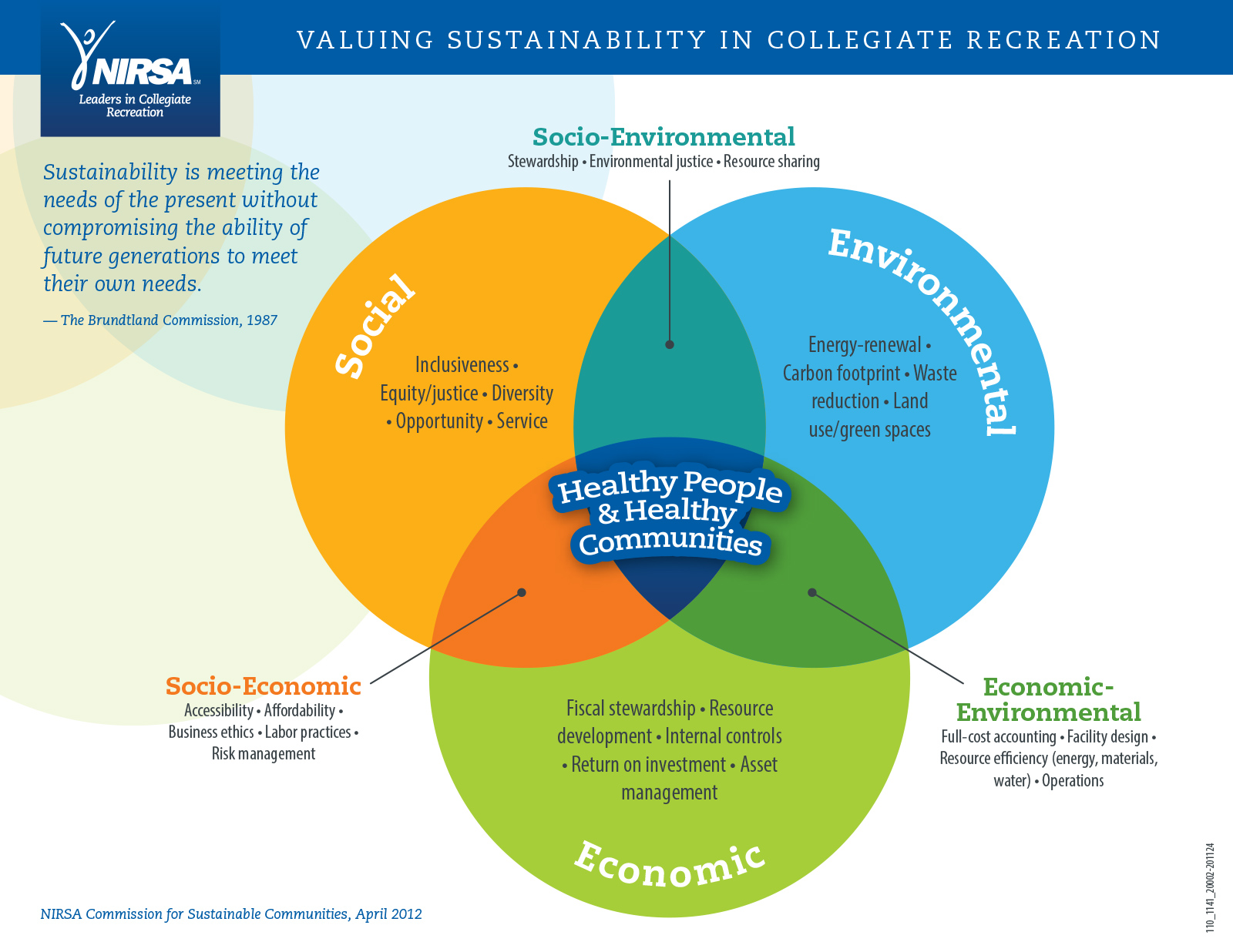

The NIRSA model “Valuing Sustainability in Collegiate Recreation” is a Venn diagram that consists of three circles, each circle representing one of the following: economic, environmental, or social considerations. The one sweet spot where these three circles overlap—where positive social, environmental, and economic actions come together—represents NIRSA’s shared vision of inspiring the development of healthy people and healthy communities worldwide.

The NIRSA model “Valuing Sustainability in Collegiate Recreation” is a Venn diagram that consists of three circles, each circle representing one of the following: economic, environmental, or social considerations. The one sweet spot where these three circles overlap—where positive social, environmental, and economic actions come together—represents NIRSA’s shared vision of inspiring the development of healthy people and healthy communities worldwide.

NIRSA’s Strategic Values Commission for Sustainable Communities has suggested that to achieve a sustainable economic model, recreation departments need to consider five key aspects that affect fiscal stewardship, resource development, internal controls, return on investments, and asset management.

But what does that all really mean in practice? As we look at our purchasing and procurement behaviors in the 2015-2016 academic year, we can take aim at that sweet spot with a few simple evolutions to our business practices. Below are some questions and ideas for you to consider in your own efforts to move your campus towards more sustainable procurement.

Fiscal Stewardship

Fiscal stewardship means using your resources within the laws, regulations, and policies of your university. It also means being transparent and having appropriate internal controls to prevent excessive financial commitments and overspending.

Is your department or program area using its financial resources responsibly? Are you buying items because your department needs them or simply to exhaust allocated funds? One way to be increasingly fiscally responsible is to evaluate your annual t-shirt overages. After the term is over, count up the remaining inventory and compare it with the past year or years; then adjust your order accordingly so you don’t have hundreds of extra shirts the next year.

Research and Development

When bidding for products or services, do you require all requests for proposals (RFP) to factor in sustainability as part of the overall selection criteria? Do you ask vendors about the amount of recycled content in their product or what they do with the product at the end of its usefulness? For example, if your department is looking for print services and you need a vendor to provide you with a bid for a copy machine(s), you could ask the vendor to address the following questions in their RFP:

- Can the machines print double-sided copies?

- Do the machines go into sleep mode when not in use to save energy?

- Does the machine function with 100% recycled paper content?

- Do they use green cleaning supplies when servicing and cleaning the machine?

- Do they recycle the ink?

- What do they do with the unit at the end of its life?

By adding or making vendors think about their sustainability practices we will continue to help all of us work towards getting these principles into the foundation of all our business practices.

Internal Controls

The internal control framework for most U.S. companies is the Committee of Sponsoring Organizations of the Treadway Commission (COSO) Internal Control—Integrated Framework, which was first issued in 1992 and updated in 2013. The framework consists of the following five pillars: control environment, risk assessment, control activities, information and communication, and monitoring. We already monitor our budgets to ensure fiscal stewardship; to make this more sustainable we would consider people, planet, and profit in our decisions.

The triple bottom line is an accounting framework that considers the three divisions of people, planet, and profit; NIRSA’s model for Valuing Sustainability in Collegiate Recreation uses the terms social, environmental, and financial, but the framework isn’t that different from the more widely known three Ps. By using the triple bottom line, the environment and the community become stakeholders in all decisions being made within your program.

Whether you are a coordinator or a director, you can monitor your business practices to ensure that you and your team are meeting all of your operational objectives. Ask questions not just about the fiscal costs/benefits, but also about the environmental and social costs/benefits as well. For example, if you’re buying a new piece of weight room equipment you would consider the following: who can use it; does it need to be inclusive so all patrons can use it; do you have pieces that can be used by everyone; does this new piece need to fit that criteria; does the company that makes the machine have sustainable practices that are in line with your program’s commitments; and lastly, how will your program benefit from this purchase?

Return on Investment

Do you want to minimize your cost and impact on the environment and maximize your return on investment (ROI)? In that case, consider not only the internal, direct costs of a purchase, but also the external cost to society. When making decisions, we need to weigh the social and environmental impacts of a purchase to ensure that one isn’t traded for another. For example, instead of raising fees which disproportionately impacts the participation of under-resourced students, consider alternate forms of revenue generation.

Asset Management

In its broadest sense, asset management is a systematic process of deploying, operating, maintaining, upgrading, and disposing of assets cost-effectively. When making major purchases do you look at the total cost of ownership, or the life-cycle cost (LCC)? In applying NIRSA’s model, you’ll see that the costs to consider are more than just the financial cost of the item; buyers also need to consider the environmental and social costs. Typical areas of expenditure which are included in calculating the LCC include: planning, design, construction and acquisition, operations, maintenance, renewal and rehabilitation, depreciation and cost of finance, and replacement or disposal.

A good example of the life cycle cost for a purchase can be seen in this sample of a dump truck purchase.

Fiscal stewardship, research and development, internal controls, ROI, and asset management work in harmony to support campus recreation programs that are sustainable and working to support the “sweet spot” of healthy people and healthy communities.

Learn More

If you would like more information, please visit one of the following resources:

- NIRSA partnered with the Higher Education Associations Sustainability Consortium (HEASC) for a webinar Student Affairs Leadership in Sustainable Purchasing and Event Coordination, April 2015. View a recording of this webinar.

- The NRDC (Natural Resources Defense Council) released the Greening Advisor in June 2014. The pages on purchasing are especially helpful, but there are many other helpful topics there as well.

We would love for this discussion to continue. If you have additional questions about sustainable purchasing and procurement, don’t forget to post them as discussion topics in the NIRSA Sustainability Community of Practice.

Or contact a member of the NIRSA Commission for Sustainable Communities.